AFT8 update version 20251024 has been released for NinjaTrader 8

Installers

- ATS Desktop installers are upgraded to support all Windows OS 64Bit, and Arm64-bit CPU chipsets, such as Surface Pro 2025 Arm64 support Windows 11 Home.

Algos – Automated trading Systems

- Algo Entry Mode – 13 – AFT000 Hybrid Algo Trader signals

Indicators

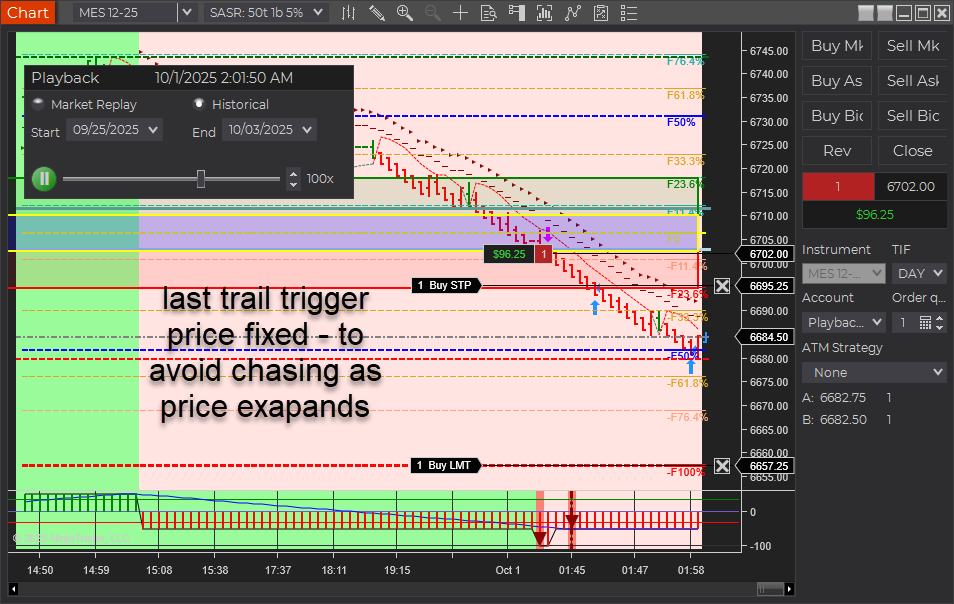

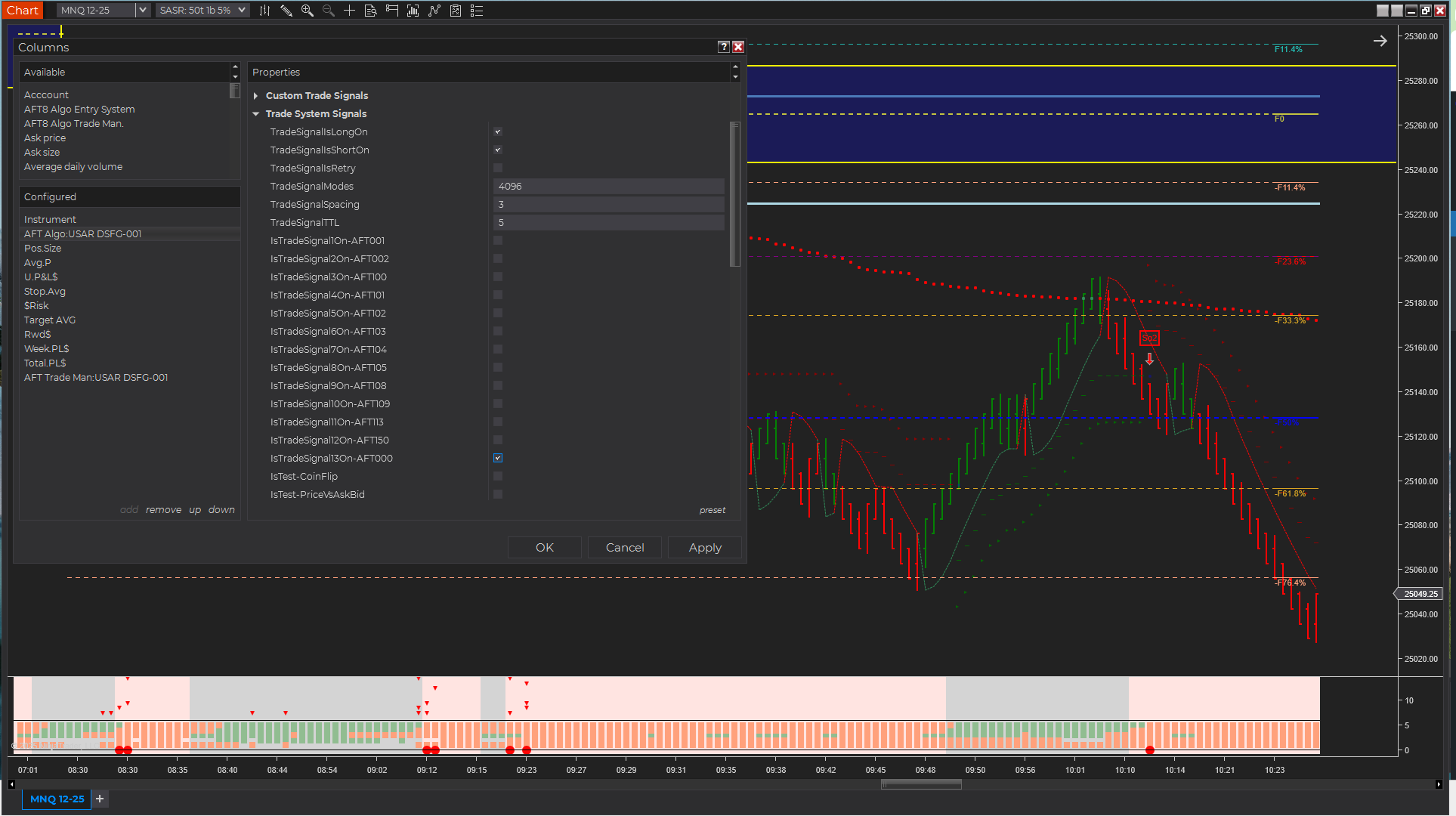

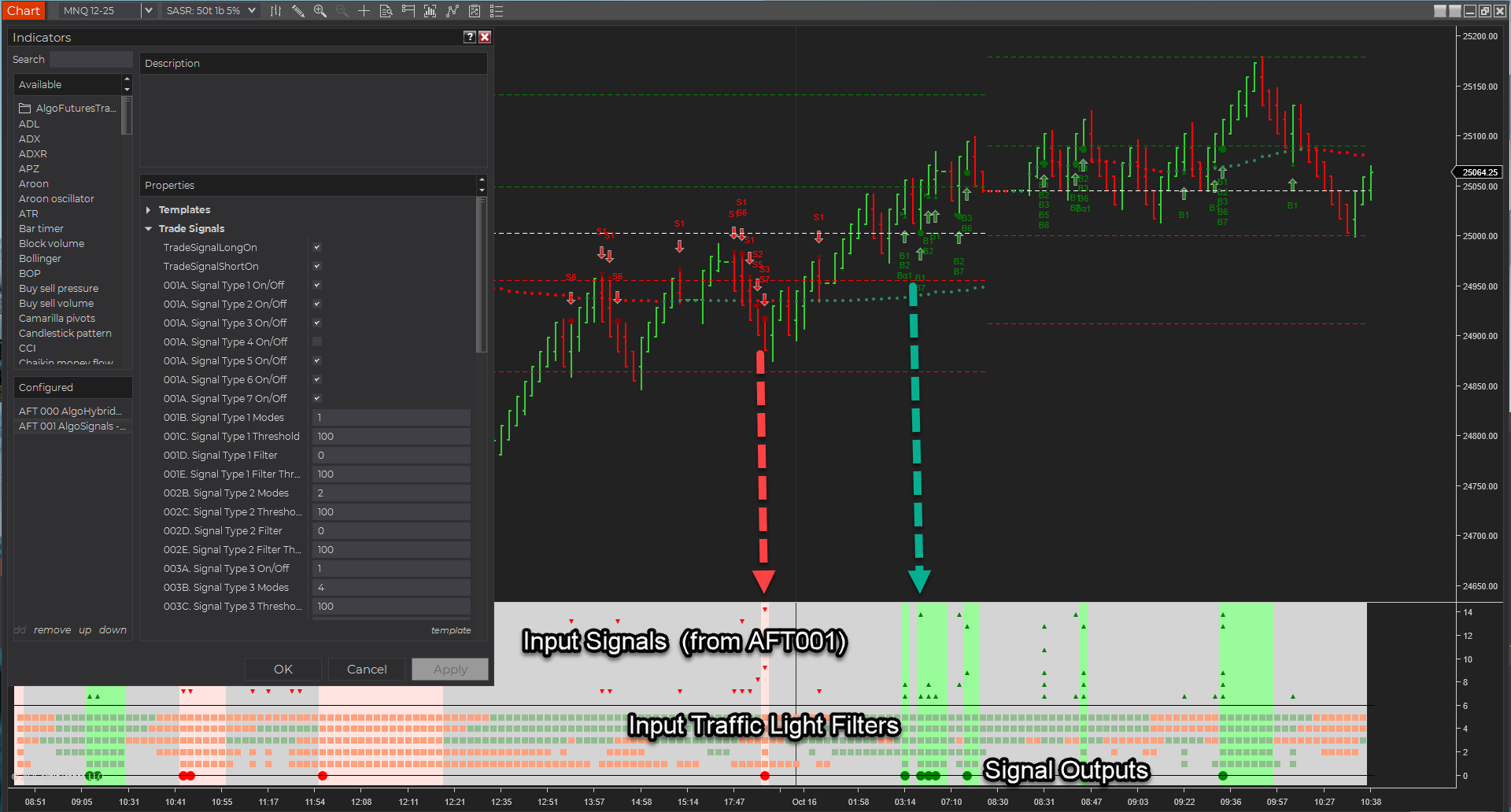

- AFT000 Hybrid Algo Chart Trader

- Programmable Signals 1 to 7

- Alpha Signals 1 to 2

- Traffic light filters

- Pending the Easy Trader NinjaBuddy GUI

Features availability and Licensing

- AFT000 access:

- requires AFT or ATS Essentials/Premium/Ultimate monthly, annual, or lifetime current and lifetime renewal

- Subscriptions & Lifetime renewals are available in ‘My Pricing’ in the ATS universal account

- AFT000 features:

- Turnkey Workspaces

- Easy Trader NinjaBuddy GUI