AFT8 version 2023.7.21 is a service release for AFT8 version 2023.7.20.

Bug Fix for System.IO.FileNotFoundException

Error: System.IO.FileNotFoundException: Could not load file or assembly ‘System.Text.Json’.

The technical reason is that some PCs were lacking resources required for .NET Standard, so parts of 2023.7.20 had to be rolled back to use backwards-compatible .NET 4.8 serialization legacy technology, Newtonsoft.

Therefore, a missing file error was logged and prevented licensing from being read and applied. Error trace: Error: System.IO.FileNotFoundException: Could not load file or assembly ‘System.Text.Json, Version=7.0.0.0, Culture=neutral, PublicKeyToken=cc7b13ffcd2ddd51’ or one of its dependencies. The system cannot find the file specified.

Apologies to those affected. It was tested on various desktops and servers and only had issues on some, hence why it slipped through the net. Lesson learned and noted so we can avoid similar issues with modern and legacy technology.

Code and Workspaces Breaking Changes and Output Changes

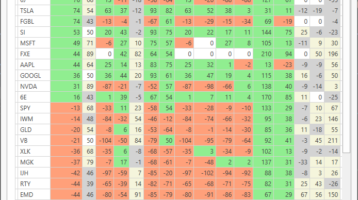

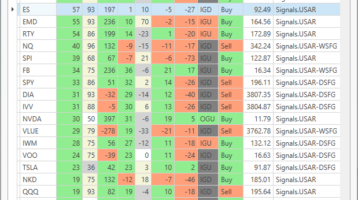

- Market Analyzer Column AFT Algo Signal Modes – now bitwise flags are used to allow multiple sets of signal indicators at the same time. Trade Signal Mode – 0: Off, 1: AFT001Algo-SignalsCombo, 2: AFT002Algo-SignalsGenerics, 4: AFT100-FibGrid, 8: AFT101-USAR, 16: AFT102-DynTrend, 1048576: SignalExec TestMode.

- All errors and output can be found in the NinjaTrader 8\Trace folder.

We are forging ahead with our other technologies. We are at the cutting edge as it has proven reliable. .NET 7.0 and now .NET 8.0 are under scrutiny. We will be moving more modules to the cloud and modern desktop, mobile, and web technologies over the course of 2023 to 2024 to minimize the impact of technology and stay ahead of the curve of any changes.